Americans Have $1.4 Trillion in Student Loan Debt—But Who Gets All That Money?

Updated: May 09, 2023

That’s more than the annual salaries of everyone who lives in Australia combined.

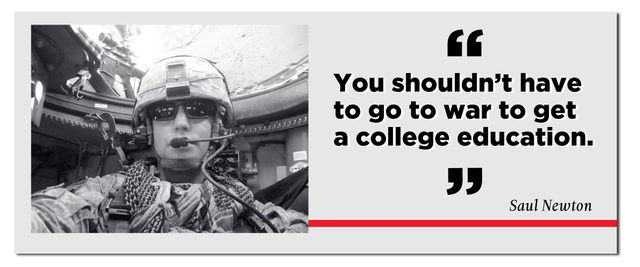

In the summer of 2010, Saul Newton was a 20-year-old rifleman stationed at a U.S. Army outpost in the remote, dangerous Arghandab River valley in Afghanistan.

It was a radical change for a kid from suburban Milwaukee, who only months before had been a student at the University of Wisconsin–Stevens Point. But after two years of tuition hikes, Newton found himself with about $10,000 in federal student loans and the prospect of borrowing still more if he stayed in school. “I couldn’t afford it anymore,” he says. He dropped out and enlisted, hoping to go back to school one day with financial help from the GI Bill. And then he went off to fight the Taliban.

But no matter what he faced in Afghanistan, once a month, Newton says, he went to the wooden shack on the outpost where the unit kept a laptop computer. That’s where he made his monthly $100 student-loan payment. He worried that if he didn’t pay his loans on time, his credit would never recover. (The government offers student-loan deferments to active soldiers in wartime, but Newton wasn’t aware of that.)

Today, back home and the executive director of the Wisconsin Veterans Chamber of Commerce, he has just made his last loan payment. However, reaching that milestone hasn’t made Newton any more optimistic about the choices other young people face, especially given the steadily rising cost of college combined with many states’ steep cuts to their education programs. “You shouldn’t have to go to war to get a college education,” he says. (These parents shared their secrets to sending their kids to college without taking out loans.)

Almost everyone knows someone like Newton, someone up to his or her neck in student-loan payments. There are roughly 44 million Americans in debt to their educations. Their average bill is $32,731. Do the math, and the country’s total school debt is a staggering $1.4 trillion. That’s more than the annual salaries of everyone who lives in Australia combined. All of which raises some obvious but often unexplored questions: Who is getting rich off of student loans? Where does all that money go?

To the colleges and universities and all the diplomas they issue, in part. But a generation ago, Congress changed the student-aid system to give private companies a piece of the action and shrink the government’s role in the process. The result has been an enormous financial windfall for Wall Street and beyond. Now just about everyone in the industry makes money off students: the banks, private investors, and even the one group Congress wanted to push out of the financial-aid business—the federal government. And the profits keep rolling in; student-loan debt generally grows by some $80 billion a year.

This is not what President Lyndon B. Johnson envisioned when he signed the Higher Education Act of 1965. Before the law, Americans who wanted to go to college had to finance it themselves. That meant paying out of their own pockets, securing scholarships, or taking out expensive private loans. After the bill, students could go to a bank for a less costly student loan guaranteed by the government. “This nation could never rest,” Johnson stressed, “while the door to knowledge remained closed to any American.”

In 1972, Congress created the Student Loan Marketing Association, or Sallie Mae, a quasi-governmental agency whose mission was to increase the amount of money available to borrow for higher education. Banks loaned money to students, and Sallie Mae bought the federally backed loans from the banks, freeing them up to lend more money. But when lawmakers turned Sallie Mae into a private company in 1996, it gained the authority to make its own loans, both federal ones guaranteed by the government and more profitable private loans, which command higher interest rates and come without governmental guarantees or restrictions.

Once only a facilitator of loans, Sallie Mae became a profiteer. And it did what it could to maximize those profits. It paid a New Jersey agency some $14 million to market Sallie Mae to colleges as their preferred campus loan provider. It paid college loan officers to serve as consultants on its advisory boards. It placed its own employees in university call centers to field questions from students who thought they were getting advice from college loan officers. Eventually, the business of collecting premiums and penalty fees was also consolidated under Sallie Mae’s very large umbrella.

Freed from governmental control, the company became a juggernaut. In 2014, it spun off most of its student-loan business into a new company, Navient, and today’s Sallie Mae handles only private loans. The most telltale sign of the company’s success: CEO Albert Lord received pay and stock totaling hundreds of millions of dollars before he retired in 2013.

Meanwhile, cash-starved states cut back funding to public universities. In turn, schools had to charge more to make up the deficit. The average annual cost of tuition, fees, and room and board at American colleges and universities rocketed from $4,563 in 1985 to $21,728 in 2015—an increase of about 13 percent a year. Over the same 30-year period, wages rose 6 percent annually at most.

If state governments had continued to support public higher education at the rate they did in 1980, they would have invested at least an additional $500 billion in their university systems, according to an analysis of data research from the U.S. Bureau of Economic Analysis. That’s roughly the amount of outstanding student debt now held by those who enrolled in public colleges and universities.

The federal government holds more than 90 percent of the $1.4 trillion in outstanding student loans, either as the original lender or the backer, making the Department of Education (DOE) effectively one of the world’s largest banks. Private lenders, including Wells Fargo, SunTrust, and other big banks, hold the rest. By the DOE’s own calculations, the government earns as much as 20 percent on each of its loans. The profit arises from the government’s ability to borrow money at a low rate and then lend it to students at a higher rate. (These are the secrets debt collectors would never tell you.)

The federal loans issued between 2007 and 2012 were projected to generate $66 billion in income for the government, according to a 2014 report from the Government Accountability Office (GAO). (In 2013, Congress lowered the interest rate for incoming student borrowers yet refused to extend the same benefit to the more than 40 million Americans who had already borrowed for their educations.)

“The United States government turns young people who are trying to get an education into profit centers to bring in more revenue for the federal government,” Sen. Elizabeth Warren said on the Senate floor in February 2016. “This is obscene. The federal government should be helping students get an education, not making a profit off their backs.”

Jessie Suren, an energetic 29-year-old who wanted a career in law enforcement, attended a free boarding school for underprivileged youth in Hershey, Pennsylvania, and then enrolled in La Salle University in Philadelphia. Scholarships didn’t cover the cost of the private college, so she borrowed about $71,000 in federal loans, much of it from Sallie Mae. A job with the U.S. Marshals Service fell through, and since graduation she has scrambled to keep current on her payments, sometimes working 16 hours a day at two low-paying jobs. She has made no headway on her loans. Just the opposite: Today her balance tops $90,000—and that figure would be higher if she’d borrowed from a private lender.

“My loans are a black cloud hanging over me,” Suren says. “I’m a student-debt slave.”

Young adults aren’t the only ones sucked into the student-loan hurricane. In 2004, Richard Brown, 66, of Ossining, New York, and his wife had good jobs in information technology. He took out $50,000 in federal student loans for his daughter. They didn’t want her to go into debt and could afford to help. But then the recession hit. Brown lost his job in 2009 and, at 58, couldn’t find another. Three years later, his wife lost her job when her company was acquired by a competitor. Their debts mounted, and by 2013, the loan balances, with compounding interest and penalties, had risen to $135,000.

The couple filed for bankruptcy, but the loans were still payable in full. Through aggressive lobbying, the banks had helped enact a law that makes student loans virtually the only consumer debt that cannot be discharged in bankruptcy except in the rarest of cases. Brown was shocked when the federal government began taking $250 a month from his Social Security check of $1,700.

“This is money we need to live on,” he says. “We worked 35 or 40 years to be eligible. I had no idea they could do that.”

In fact, the government can take as much as 15 percent of a debtor’s Social Security. In 2013, the government garnished the benefits of 155,000 Americans who were in default on their federal student loans, according to a GAO report, up from 31,000 in 2002. This policy of withholding federal payments to delinquent borrowers, known as administrative offset, can also apply to tax refunds and disability checks.

Today, one in four borrowers is behind in his or her payments or is struggling to make them, according to the Consumer Financial Protection Bureau, which estimates that nearly 8 million loans are in default. The number of federal loans in default jumped 14 percent from 2015 to 2016, according to an analysis by the Consumer Federation of America.

For all it has invested in the student-loan program, the government doesn’t have the resources to hunt down all the people who are behind on their payments. Since 1981, the DOE has hired debt collectors to do the dirty work—on the taxpayers’ dime. For fiscal 2016, officials estimated that these contractors would receive $2.1 billion in commissions on the money they’d recover from borrowers in default.

Ironically, as Jessie Suren scrambled to pay back her loans, one of her jobs was to try to get money out of people who were delinquent on their student loans. She was paid $12 an hour at a call center in Harrisburg, Pennsylvania. Some of the calls were scary, she says; angry borrowers would curse and threaten her, declaring they were jobless and broke. Other calls were heartbreaking; borrowers would claim they or their children were terminally ill.

Whatever their story, Suren had to tell them what would happen if they didn’t pay: The company could garnish their wages and take their tax refunds. After hanging up, Suren would sometimes reflect on her own student loans, thinking, This is going to be me in a couple of years.